Turning 30 can make money feel more serious, but setting financial goals before 30 is not about having everything perfectly figured out.

It is about learning how to manage your money with more intention so your future feels less stressful. A lot of people reach their late 20s and suddenly start thinking about savings, debt, income, career growth, investing, retirement goals by age, buying a home, travel, family responsibilities, or long-term financial stability.

At the same time, it is easy to feel behind. Social media can make it look like everyone else is buying a house, investing every month, building a business, or reaching huge money goals before 30.

But real financial progress is usually quieter than that. It often looks like tracking your spending, saving a little more than last month, paying down one balance, saying no to a purchase that does not match your priorities, or finally creating a financial plan you can actually follow.

That is why realistic financial goals matter. The goal is not to copy someone else’s money timeline. The goal is to create a system that fits your income, your responsibilities, your lifestyle, and the life you are trying to build.

Quick Answer: What Financial Goals Should You Set Before 30?

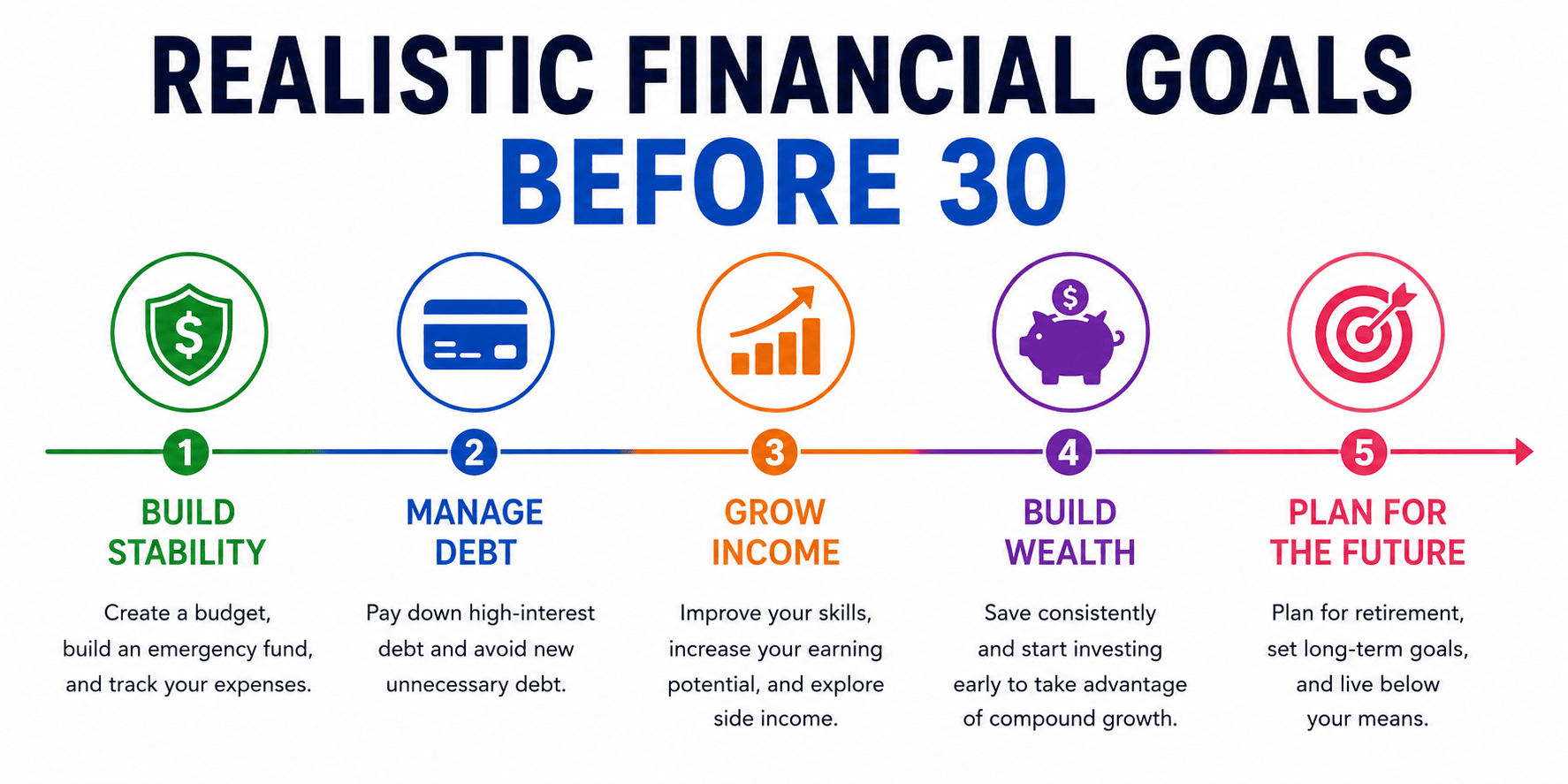

Before turning 30, realistic financial goals may include building an emergency fund, creating a monthly budget, paying down high-interest debt, improving income skills, learning about investing, and setting both short-term financial goals and long-term financial goals.

If you are still learning how to organize your money, start with the basics first. A guide like what is a good monthly budget can help you understand how your income should be divided before you move into bigger goals like investing or retirement planning.

The most important part is not choosing impressive goals. It is choosing smart financial goals that match your real situation.

- Short-term goals: emergency savings, budgeting goals, debt payoff, expense tracking, and saving for near-future needs.

- Long-term goals: retirement planning, investing, home savings, career growth, financial independence, and building wealth gradually.

- Personal money goals: reducing stress, creating freedom, supporting family, traveling responsibly, or preparing for independence.

Quick Navigation

- Why financial goals matter before 30

- Start with your real financial situation

- Short-term financial goals to build first

- Long-term financial goals to prepare for

- How to create a realistic financial plan

- Build an emergency fund

- Create budgeting goals you can follow

- Pay down high-interest debt

- Improve your income skills

- Learn goal investing without rushing

- Stop comparing your financial timeline

- Common mistakes when setting financial goals

- Related tools

- Related guides

- Frequently asked questions

Why Financial Goals Matter Before 30

Your 20s are usually the stage where money habits start becoming long-term patterns. This is often when you begin earning your own income, managing bills, handling debt, making bigger spending decisions, and thinking more seriously about the future.

Without financial goals, money can disappear without a clear purpose. You may earn income every month but still feel like you are not moving forward because there is no plan telling your money where to go.

Setting financial goals gives your money direction. Instead of only reacting to bills and impulse purchases, you start deciding what your income should help you build.

That could mean building peace of mind, paying off debt, saving for travel, moving out, investing for the future, supporting family, starting a business, or preparing for retirement slowly.

The real goal of financial planning: Your financial plan should help you feel more prepared, not more pressured.

This is why realistic goals matter more than perfect goals. A realistic goal challenges you, but it does not make you feel like a failure every time life gets expensive or unpredictable.

A realistic financial plan before 30 usually starts with stability first, then grows into debt payoff, income growth, investing basics, and long-term financial goals.

Start With Your Real Financial Situation

One of the biggest mistakes people make is setting financial goals based on internet pressure instead of their real life.

A financial goal that sounds good online may not make sense for your income, location, debt, family responsibilities, career stage, or cost of living.

Before creating a financial plan, review your current situation honestly. If you do not know where your money is going, start by reading how to track expenses or use an expense tracker calculator to see your real spending patterns.

- How much do you earn in an average month?

- Is your income stable or irregular?

- How much do you spend on fixed expenses?

- How much do you spend on flexible expenses?

- Do you have high-interest debt?

- Do you already have emergency savings?

- Do you support anyone financially?

- What financial problem causes the most stress right now?

These questions matter because financial goals should solve real problems in your life. If your biggest stress is not having emergency money, then building savings may be more important than investing right away. If your biggest stress is credit card debt, then debt payoff may deserve more attention than saving for a vacation.

Realistic financial goals should make your life more stable one step at a time.

Short-Term Financial Goals to Build First

Short-term financial goals are money goals you can usually work on within a few weeks, months, or one to two years.

These goals matter because they create momentum. You do not need to wait ten years to feel progress. Small wins can help you stay motivated and build confidence.

Save your first emergency fund

Start with a small target if a full emergency fund feels overwhelming. Even a small buffer can help prevent new debt.

Track your spending for 30 days

Before changing your entire budget, learn where your money is actually going.

Pay off one small balance

Clearing one debt can create motivation and make your financial plan feel more achievable.

Create a monthly budget

A simple monthly budget can help you organize income, bills, savings, and guilt-free spending.

Short-term goals may seem simple, but they are important. They help you stop guessing and start building structure around your money.

Long-Term Financial Goals to Prepare For

Long-term financial goals are bigger goals that usually take several years or even decades. These may include investing, retirement planning, buying a home, building wealth, becoming debt-free, starting a business, or reaching financial independence.

Before turning 30, you do not need to complete every long-term goal. The better goal is to start preparing for them.

For example, retirement goals by age can feel intimidating when you are still trying to stabilize your monthly budget. But you can start small by learning about retirement accounts, compound growth, employer benefits, or beginner investing options available in your country.

Long-term planning does not have to be dramatic. It can begin with small actions:

- learning how investing works,

- saving consistently every month,

- avoiding unnecessary lifestyle inflation,

- building career skills that increase income,

- and creating a habit of planning before spending.

The earlier you build these habits, the easier your 30s can feel financially.

How to Create a Realistic Financial Plan Before 30

A financial plan does not need to be complicated. It simply needs to show what your money is doing now, what you want it to do next, and what steps you will take to move closer to your goals.

Choose your top three priorities

Do not try to fix everything at once. Choose the three goals that would make the biggest difference in your current life.

Give each goal a number

Instead of saying “save more money,” choose a clear number such as saving $1,000 or paying off $500 of debt.

Set a realistic timeline

A goal becomes easier to follow when you know whether you are working on it for three months, six months, one year, or longer.

Review your progress monthly

Your financial plan should be flexible. Review it often and adjust when your income, expenses, or priorities change.

This is where smart financial goals can help. A SMART goal is specific, measurable, achievable, relevant, and time-based. That may sound formal, but it simply means your goal should be clear enough to follow.

For example, “I want to be better with money” is vague. “I want to save $1,200 for emergencies in the next 12 months by saving $100 per month” is much easier to act on.

1. Build an Emergency Fund

An emergency fund is one of the most important financial goals before turning 30 because it protects you from unexpected expenses.

Life can change quickly. Job loss, medical expenses, urgent travel, car repairs, home repairs, family needs, or income delays can happen even when you are careful with money.

Without emergency savings, even a small problem can become debt. That is why emergency money is not just a savings goal. It is a stress-reduction goal.

You can estimate your target using an emergency fund calculator or create a specific savings timeline with a savings goal calculator.

If you want to understand how much of your income should go toward saving each month, you can also read how much should you save each month.

2. Create Budgeting Goals You Can Actually Follow

Budgeting goals should not make your life feel miserable. A budget should help you feel more organized, not constantly restricted.

If you are not sure where to start, you can use a monthly budget calculator, a 50/30/20 budget calculator, or a zero-based budget calculator to test different budgeting styles.

A realistic budget usually includes:

- necessities,

- debt payments,

- emergency savings,

- future goals,

- personal spending,

- and occasional fun.

Many people quit budgeting because they make the system too strict. If your budget removes all enjoyment, you may eventually overspend because you feel deprived.

This is also why many budgets fail. If you keep restarting your plan every month, this guide on why most budgets fail and how to fix yours can help you make your system more realistic.

3. Pay Down High-Interest Debt

High-interest debt can slow down your financial progress because interest keeps adding to your balance.

Start by listing each debt, the balance, the interest rate, and the minimum payment. If you are unsure how serious your debt load is, use a debt-to-income ratio calculator or read how much debt is too much.

If credit card debt is part of the problem, this guide on what happens if you only pay the minimum on credit cards can help you understand why minimum payments can keep you stuck longer than expected.

You can also compare payoff plans using a debt payoff snowball calculator, a loan debt payment calculator, or a credit card payment calculator.

If you are trying to decide whether to save first or attack debt first, read is it better to pay off debt or save money first.

4. Improve Your Income Skills

Saving money matters, but increasing your earning potential also matters. There is only so much you can cut from your budget, especially if your income is already tight.

Before turning 30, one of the smartest financial goals is improving skills that can help you earn more over time.

Income-building skills may include:

- communication,

- writing,

- sales,

- marketing,

- project management,

- data analysis,

- coding,

- design,

- leadership,

- remote work tools,

- or freelance client management.

You do not need to chase every trend. Choose skills that match your personality, career direction, and financial goals.

A small increase in income can make a big difference when you also manage your money well.

5. Learn Goal Investing Without Rushing

Investing is one of the most common long-term financial goals, but it can feel overwhelming when you are still trying to build savings or pay debt.

Before investing aggressively, it usually helps to build a foundation first: basic emergency savings, a clear budget, reduced high-interest debt, and an understanding of your risk tolerance.

If you are ready to explore investing, you can start with an investment growth calculator, a compound interest calculator, or a investment goal calculator to see how time, contributions, and returns can affect long-term goals.

If retirement is one of your long-term goals, you can also use a retirement savings calculator or a retirement goal calculator to estimate what you may need later.

Stop Comparing Your Financial Timeline

One of the hardest parts of setting financial goals before 30 is not the math. It is the comparison.

Some people have family support. Some have no debt. Some live in lower-cost areas. Some earn high salaries early. Some inherit money. Some have fewer responsibilities. Some are struggling quietly even if their life looks successful online.

Your financial plan should not be based on someone else’s starting point.

For one person, success before 30 may be buying a home. For another person, it may be becoming debt-free. For someone else, it may be finally building emergency savings after years of instability.

None of those goals are automatically better than the others. What matters is whether your financial life is moving in a healthier direction.

Common Mistakes When Setting Financial Goals

Setting goals is helpful, but some mistakes can make the process harder than it needs to be.

Setting goals that are too extreme

If your goal requires you to change everything overnight, it may not be sustainable.

Ignoring irregular expenses

Birthdays, holidays, repairs, medical costs, and annual fees can ruin a budget if you never plan for them.

Trying to do everything at once

Saving, investing, paying debt, and increasing income all matter, but you may need to focus on one or two priorities first.

Waiting for the perfect time

You do not need perfect income or perfect knowledge to start improving your money habits.

Frequently Asked Questions

What financial goals should I set before turning 30?

Good financial goals before turning 30 include building emergency savings, creating a realistic budget, paying down high-interest debt, improving income skills, learning about investing, and setting long-term financial goals.

What are examples of short-term financial goals?

Short-term financial goals include saving your first emergency fund, paying off one small debt, tracking expenses, creating a monthly budget, or saving for a planned purchase.

What are examples of long-term financial goals?

Long-term financial goals include retirement planning, investing consistently, buying a home, becoming debt-free, building wealth, or creating multiple income streams.

How do I create smart financial goals?

Make your goal specific, measurable, realistic, relevant, and time-based. Instead of saying “I want to save money,” say “I want to save $1,200 in 12 months by saving $100 per month.”

Should I save money or pay off debt first?

Many people benefit from doing both. A small emergency fund helps prevent new debt, while a debt payoff plan reduces interest and financial stress over time.

Is it too late to start financial planning in my late 20s?

No. Your late 20s are still a strong time to improve your financial habits. Even a few years of consistent budgeting, saving, debt payoff, and income growth can make your 30s more stable.

Important Note

This guide is for educational purposes only and should not be taken as personal financial advice.

Financial goals depend on your income, expenses, debt, location, family responsibilities, risk tolerance, and long-term plans. Adjust any example to fit your real situation.