Budgeting your salary sounds simple until payday arrives and your money already has too many jobs. Food, rent, electricity, water, internet, mobile load, commute, debt, family help, school expenses, medicines, and emergencies can make your salary feel smaller than it looked on paper.

That is why a good salary budget in the Philippines should not be copied blindly from a foreign personal finance video. The basic idea of dividing money into needs, wants, and savings is useful, but the percentages need to fit your real life. A person living with family has a different budget from someone renting in Metro Manila. A single employee has a different situation from someone supporting parents, siblings, or children.

This guide will show you how to divide your salary in a practical way, how to adjust the 50/30/20 rule when it does not fit, how to build savings even with a small income, and how to avoid common payday mistakes. You can also use the monthly budget calculator or the 50/30/20 budget calculator to test your own numbers.

Quick Answer Summary

- Start with take-home pay, not gross salary. Budget the money that actually reaches your account.

- Separate needs, wants, and savings on payday. Do not wait until the end of the month to see what is left.

- Use 50/30/20 as a guide, not a strict rule. Filipino budgets often need adjustment because food, rent, transport, and family responsibilities vary widely.

- Save something, even if it is small. Consistency matters more than starting with a perfect amount.

- Track your spending for one month. Most budgeting problems become clearer when you see where the money actually goes.

Quick Navigation

- Why budgeting your salary feels hard in the Philippines

- What needs, wants, and savings really mean

- Start with your real take-home pay

- A realistic salary budget formula

- Sample salary budget breakdowns

- How to budget a ₱20,000 salary

- How to budget a ₱30,000 salary

- Budgeting with a small salary

- How to budget when you support family

- How much to save from your salary

- A simple payday system

- Common budgeting mistakes

- Warning signs your budget is not working

- Practical budgeting tips for Filipino workers

- Related calculators

- Related guides

- Sources and editorial note

- FAQ

Why Budgeting Your Salary Feels Hard in the Philippines

Budgeting is not hard because people are careless. Often, it is hard because the salary has to stretch across too many responsibilities. One payday can already include groceries, rent, electricity, internet, transport, debt payments, school needs, medicine, family help, and a few personal expenses you have been postponing for weeks.

In the Philippines, budgeting also changes depending on where you live. Someone working in a city may spend more on rent and commuting. Someone living with family may spend less on rent but more on household contributions. Some workers receive fixed monthly pay, while others rely on commissions, overtime, freelance income, or irregular business income.

There is also the emotional side of money. After working hard, it is normal to want a nice meal, a small Shopee or Lazada order, coffee, skincare, clothes, or a weekend treat. The goal of budgeting is not to remove every enjoyable thing from your life. The goal is to stop your money from disappearing without a plan.

Realistic mindset: a budget should help you make better decisions, not make you feel guilty for being human. A plan that is too strict usually breaks after one stressful week.

What Needs, Wants, and Savings Really Mean

The needs, wants, and savings method works because it gives every peso a clear role. Instead of seeing your full salary as spending money, you divide it into three main groups.

Needs

Needs are expenses required to live, work, stay healthy, and keep your responsibilities current. This includes food, rent, utilities, transport, debt minimums, basic healthcare, insurance, school expenses, and family support you truly need to give.

Wants

Wants are expenses that improve comfort or enjoyment but are not required for survival. This includes eating out, online shopping, streaming subscriptions, milk tea, coffee runs, gaming, beauty products, travel, and non-essential upgrades.

Savings

Savings include emergency funds, sinking funds, future purchases, investments, retirement savings, and money set aside for upcoming expenses like birthdays, school enrollment, repairs, or medical needs.

Debt Payments

Debt can be part of needs if it is a required monthly payment. Extra debt payments can be placed under savings or financial goals because they improve your future cash flow.

The tricky part is that some expenses can move between categories. A basic phone plan used for work is a need. A more expensive plan for convenience may be partly a want. Groceries are a need, but expensive snacks and impulse buys may be wants. Budgeting improves when you become honest about these gray areas without being too harsh on yourself.

Start With Your Real Take-Home Pay

Before dividing your salary, use your take-home pay instead of your gross salary. Gross salary is the amount before deductions. Take-home pay is the money you actually receive after deductions such as tax, SSS, PhilHealth, Pag-IBIG, loan deductions, or company-related deductions.

For example, if your gross salary is ₱30,000 but only ₱26,500 reaches your payroll account, build your budget around ₱26,500. If you budget based on ₱30,000, your plan will already be short before the month starts.

- Check your payslip. Look at the net pay or actual deposited amount.

- List fixed deductions. Include government deductions, loans, cash advances, and automatic payments.

- Use the amount you can control. This is the money you divide into needs, wants, and savings.

- Adjust for pay schedule. If you are paid twice a month, decide which bills come from each payday.

If you want a clearer monthly view, use the monthly budget calculator to list income and expenses in one place.

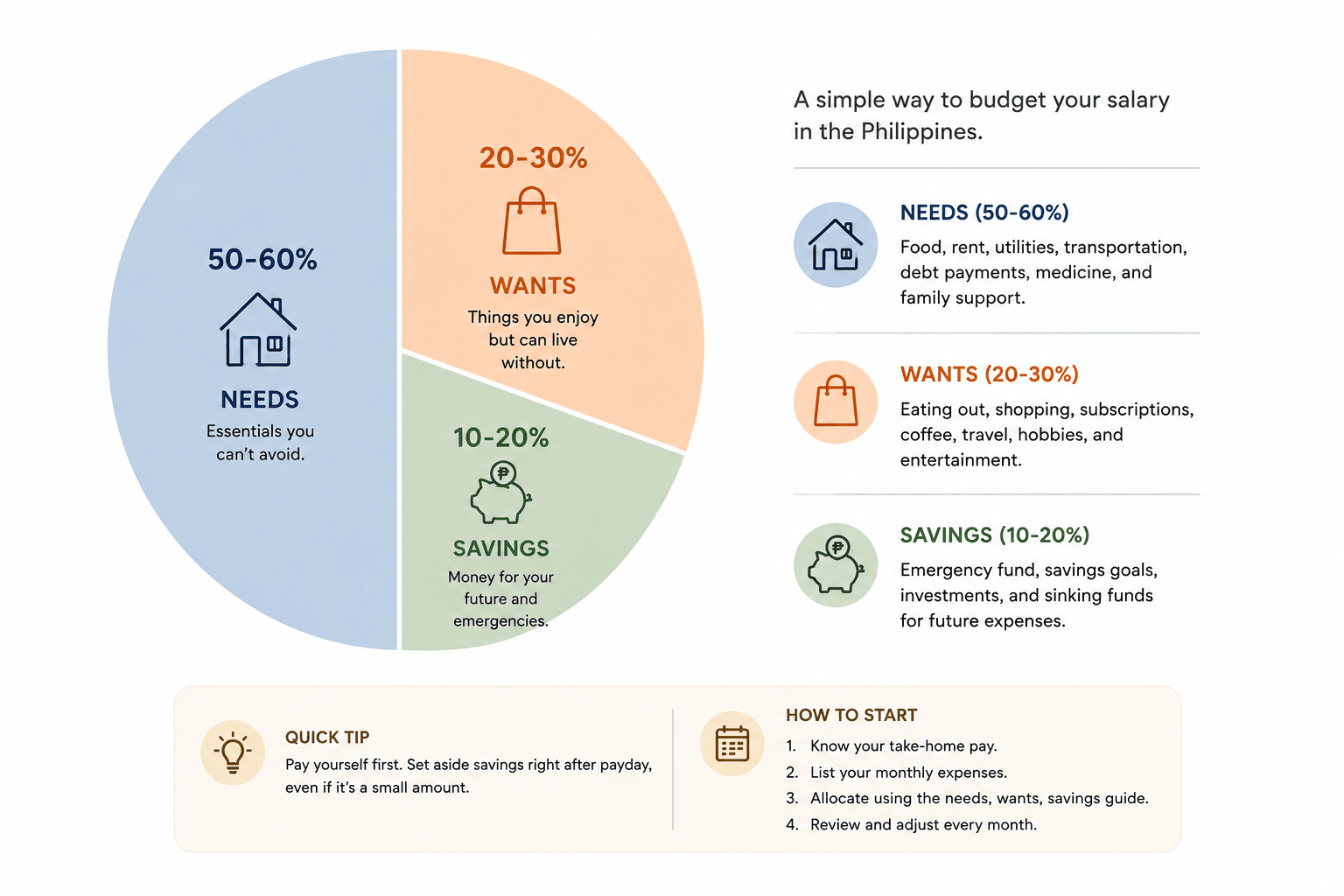

A simple visual example of how many Filipinos divide their salary into needs, wants, and savings depending on their income and responsibilities.

A Realistic Salary Budget Formula for Filipinos

The popular 50/30/20 rule divides income into 50% needs, 30% wants, and 20% savings. It is simple and useful, but it may not fit everyone in the Philippines. If rent, food, commuting, family support, or debt already takes more than half your salary, forcing the exact rule can make you feel like you are failing.

| Budget Type | Suggested Range | Best For |

|---|---|---|

| Classic 50/30/20 | 50% needs, 30% wants, 20% savings | People with stable income and manageable fixed expenses |

| Practical Filipino version | 60% needs, 20% wants, 20% savings | People with higher living costs but still able to save well |

| Tight budget version | 70% needs, 20% wants, 10% savings | People with lower income, debt, or family obligations |

| Survival season version | 80% needs, 15% wants, 5% savings | People trying to stay afloat while still building the habit of saving |

The best formula is not always the one with the highest savings percentage. The best formula is the one you can repeat without borrowing before the next payday.

Sample Salary Budget Breakdowns

These examples are not rules. They are starting points. Your real budget may be different depending on rent, location, dependents, debt, transportation, and lifestyle.

| Monthly Take-Home Pay | Needs | Wants | Savings |

|---|---|---|---|

| ₱15,000 | ₱10,500 | ₱3,000 | ₱1,500 |

| ₱20,000 | ₱13,000 | ₱4,000 | ₱3,000 |

| ₱30,000 | ₱18,000 | ₱6,000 | ₱6,000 |

| ₱50,000 | ₱27,500 | ₱10,000 | ₱12,500 |

A ₱15,000 salary may not realistically save 20% if the person pays rent, transport, and family support. In that case, saving ₱500 to ₱1,000 consistently is still progress. The goal is to build the habit first, then increase the amount when possible.

How to Budget a ₱20,000 Salary in the Philippines

A ₱20,000 monthly salary can work, but it needs boundaries. The biggest challenge is that one or two expenses can easily take over the budget. Rent, debt, food, or commuting can quickly reduce what is left.

| Category | Sample Amount | Notes |

|---|---|---|

| Food and groceries | ₱5,000 | Adjust depending on household size and whether you cook or buy meals |

| Rent or household share | ₱4,000 | Can be higher in cities or lower if living with family |

| Transport | ₱2,500 | Commute costs can change a lot by location and work schedule |

| Utilities and phone | ₱2,000 | Electricity, water, internet share, mobile data |

| Family support or debt | ₱2,000 | Keep this planned so it does not surprise the rest of the budget |

| Wants | ₱2,500 | Eating out, shopping, subscriptions, small treats |

| Savings | ₱2,000 | Emergency fund or short-term savings goal |

With this income level, budgeting becomes easier when you plan wants clearly. Without a wants limit, small purchases can quietly eat the savings category.

How to Budget a ₱30,000 Salary in the Philippines

A ₱30,000 salary gives more room, but it can still disappear quickly if lifestyle spending rises at the same time. This is where many people experience lifestyle creep. The salary increases, but savings do not improve because eating out, subscriptions, shopping, and convenience spending also increase.

| Category | Sample Amount | Budget Role |

|---|---|---|

| Needs | ₱18,000 | Rent, food, bills, transport, debt, basic responsibilities |

| Wants | ₱6,000 | Dining out, subscriptions, shopping, entertainment |

| Savings | ₱6,000 | Emergency fund, sinking funds, investments, future goals |

If you have debt, you can split the savings category into emergency savings and extra debt payment. For example, ₱3,000 for emergency fund and ₱3,000 for extra debt payment. If you already have an emergency fund, more of that amount can go toward investments or long-term goals.

Budgeting With a Small Salary

If your salary is small, the advice “just save 20%” can feel unrealistic. When most of your income goes to food, commute, bills, and family needs, saving a big amount may not be possible yet. That does not mean budgeting is useless. It means your first goal is control and stability.

- Track where your money goes for one full month.

- Separate bills immediately after payday.

- Save a small fixed amount first, even ₱100, ₱300, or ₱500.

- Reduce one repeated spending leak instead of trying to cut everything.

- Avoid borrowing for wants, even small wants.

- Build a tiny emergency fund before aggressive investing.

The first win is not becoming rich immediately. The first win is reaching the next payday without panic borrowing. Once that becomes normal, you can slowly increase savings.

How to Budget When You Support Family

Many Filipino workers help family members. This can be a beautiful responsibility, but it needs a clear budget. Without a limit, family support can become unpredictable and make it harder to pay your own bills or build savings.

A practical approach is to decide a fixed monthly amount for family support. Treat it like a planned category, not a surprise expense every week. If someone asks for extra help, check your emergency fund and other obligations before saying yes.

Helpful boundary: generosity is good, but it should not always require financial self-destruction. A sustainable support amount is better than giving too much one month and borrowing the next.

If family needs are unpredictable, create a small family sinking fund. This is separate from your personal emergency fund and can help cover medicine, school needs, small repairs, or urgent requests.

How Much Should You Save From Your Salary?

A good savings target depends on your income and responsibilities. If you can save 20%, that is strong. If you can only save 5% right now, that is still better than saving nothing. What matters is that you build the habit and protect the money after saving it.

Beginner Target

Save 5% to 10% of take-home pay if your budget is tight. This is useful for building the habit without making the rest of your budget impossible.

Stronger Target

Save 15% to 20% if your needs are under control and you do not have heavy high-interest debt.

Emergency Fund Goal

Build at least one month of basic expenses first, then work toward three to six months over time.

Sinking Funds

Save monthly for predictable expenses like Christmas, birthdays, school enrollment, insurance, repairs, and medical costs.

If you want to estimate a specific savings target, use the savings goal calculator or the emergency fund calculator.

A Simple Payday Budgeting System

The best time to budget is payday, before the money starts moving. If your salary stays in one account with no plan, it is easy to overspend because the balance looks bigger than it really is.

- Move bill money first. Set aside rent, utilities, debt payments, and required expenses.

- Transfer savings immediately. Even a small automatic transfer helps protect savings from impulse spending.

- Separate daily spending money. Decide how much you can spend until the next payday.

- Create a wants allowance. Give yourself a guilt-free amount for non-essentials.

- Check the plan weekly. A quick review prevents surprises before the next payday.

You can do this with separate bank accounts, e-wallet pockets, envelopes, a spreadsheet, or a notes app. The tool matters less than the habit of separating money before spending begins.

Common Budgeting Mistakes

Budgeting Gross Salary

This makes your plan look better than reality. Always use take-home pay.

Saving What Is Left

If savings waits until the end of the month, there may be nothing left. Save first, even a small amount.

No Wants Category

A budget with no room for enjoyment often leads to guilt spending later.

Ignoring Small Purchases

Snacks, delivery fees, coffee, subscriptions, and small online orders can add up quickly.

No Emergency Fund

Without emergency savings, one unexpected expense can turn into debt.

Copying Someone Else’s Budget

Your budget should match your salary, city, family responsibilities, and real expenses.

Warning Signs Your Budget Is Not Working

- You regularly borrow before the next payday.

- Your bills are paid, but savings never happens.

- You do not know where your money went.

- You keep using credit or loans for normal spending.

- You feel guilty every time you spend, even on needs.

- Your wants category is secretly bigger than your needs category.

- You have no money set aside for predictable annual expenses.

If several of these feel familiar, do not start by blaming yourself. Start by tracking one month honestly. A real budget is built from your actual habits, not from what you wish your spending looked like.

Practical Budgeting Tips for Filipino Workers

Plan Around Paydays

If you are paid twice a month, assign specific bills to each payday so one cutoff does not carry everything.

Use Sinking Funds

Save little by little for Christmas, school expenses, insurance, birthdays, travel, and repairs.

Keep Wants Visible

Track lifestyle spending separately so it does not hide inside groceries or daily cash withdrawals.

Give Every Peso a Job

Unassigned money usually becomes impulse spending. Decide where it should go before it disappears.

Review Prices Monthly

Food, fuel, rent, and transport costs can change. Update your budget when real prices change.

Protect Your Emergency Fund

Keep emergency money separate from daily spending so it does not feel available for wants.

One Simple Way to Separate Needs, Wants, and Savings

One reason budgeting feels difficult is because everything stays in one balance. When your bills money, spending money, savings, and extra cash are all mixed together, it becomes harder to tell what is actually safe to spend.

Some people find it easier to follow the 50/30/20 budgeting method by separating money into different apps or accounts right after payday. It does not need to be complicated. Even having one place for savings and another for daily spending can already make budgeting feel more organized.

Some links below may be referral links. If you sign up through them, LifeToolSuit may receive a small reward at no extra cost to you.

| App or Bank | Simple Budget Use | How Some People Use It | Referral |

|---|---|---|---|

| GoTyme Bank | Savings goals, separated spending money, and budgeting categories | Some people prefer using a separate digital bank account for savings or for money they do not want mixed with daily spending. |

GET GOTYME APP

Use Code: GOTYPH2XXX |

| MariBank | Emergency savings or future goal money | Keeping savings separate can make it feel less tempting to spend before the next payday. |

GET MARIBANK APP

Get ₱150 with Code CP661878 |

| Maya | Budget tracking, bills, savings, and online payments | Some people like using Maya to separate bills money from everyday spending or savings goals. |

GET MAYA APP

Get ₱50 with Code @clarissa0225 |

Simple budgeting habit: many people budget better when they stop treating their whole salary as one spending balance. Separating money into categories can make it easier to avoid overspending before the next payday.

Sources and Editorial Note

This guide was written for general educational purposes and should not be treated as personal financial advice. Salary, family responsibility, debt, and living costs vary widely, so use the examples as planning references rather than fixed rules.

- National Wages and Productivity Commission, Department of Labor and Employment: regional wage information and wage orders.

- Philippine Statistics Authority: Consumer Price Index and inflation reports.

- Bangko Sentral ng Pilipinas: financial inclusion resources and consumer finance information.

Editorially, this page focuses on realistic budgeting behavior instead of perfect percentages. The goal is to help readers create a salary system they can actually follow.

Frequently Asked Questions

How should I budget my salary in the Philippines?

Start with your take-home pay. Set aside money for needs first, then savings, then wants. If your salary is tight, use flexible percentages instead of forcing the exact 50/30/20 rule.

Is the 50/30/20 rule realistic in the Philippines?

It can be realistic for some people, but not everyone. If rent, food, transport, or family support takes a large part of your income, a 60/20/20 or 70/20/10 version may be more practical.

How much should I save from my salary?

If possible, aim for 10% to 20%. If your budget is tight, start with 5% or any fixed amount you can repeat every payday.

Should I save money if I still have debt?

It is usually helpful to keep at least a small emergency fund while paying debt. Without savings, one unexpected expense can push you back into borrowing.

How do I stop overspending after payday?

Separate your money immediately. Move bills, savings, and daily spending into different accounts, envelopes, or categories before you start spending.

What if my salary is too small to save?

Start with a very small amount. Even ₱100 or ₱300 per payday can build the habit. Then look for one spending leak to reduce gradually.

Should family support be part of needs or wants?

If it is a regular responsibility, treat it as a need and give it a clear monthly limit. This keeps your budget honest and prevents surprise shortfalls.

What is the best budgeting method for Filipino workers?

The best method is the one you can follow consistently. A flexible needs, wants, and savings system works well because it is simple and easy to adjust.