Living with my parents completely changed the way I think about budgeting, saving money, and spending intentionally.

A lot of people assume that if you live at home, you automatically spend your income carelessly because you have fewer bills. But for me, it became the opposite.

I realized that living with my parents gave me a rare opportunity to build financial stability earlier than I probably could if I were already paying rent, groceries, transportation, utilities, and every other monthly expense independently.

Instead of treating my salary like unlimited spending money, I started becoming more intentional about where every part of my income goes each month.

Over time, I created a simple budgeting system that helps me save aggressively, support my family, prepare for emergencies, and still enjoy life without feeling guilty every time I spend money.

This system may not work for everyone, but it works well for my current season of life and helped me become much more disciplined with money.

Instead of treating my salary like unlimited spending money, I created a monthly budget system that helps me:

- save aggressively,

- support my family,

- prepare for emergencies,

- and still enjoy life without guilt.

This is not meant to be the perfect salary budget for everyone. This is simply how I budget my salary based on my current season of life.

Quick Answer: How I Budget My Salary

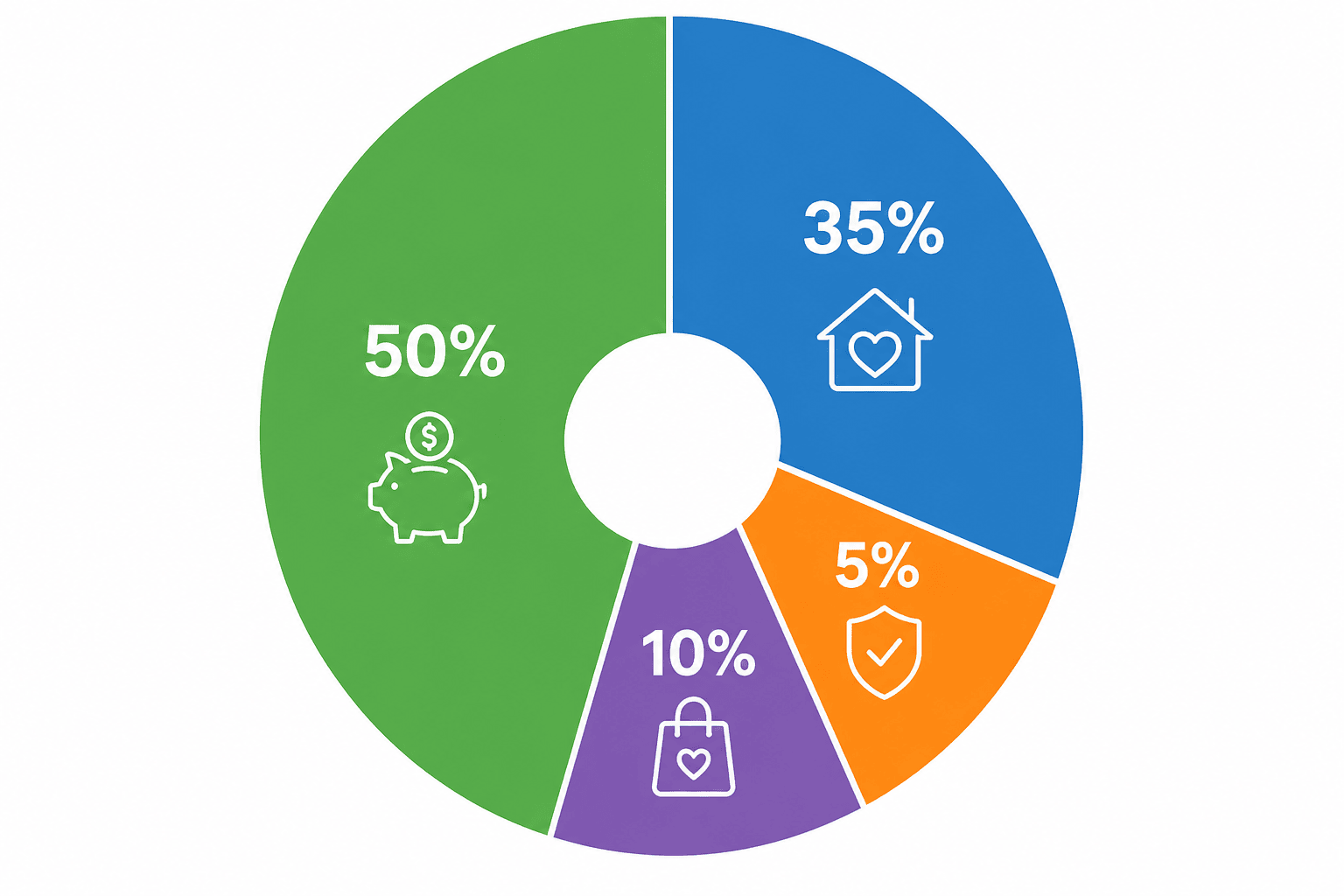

I budget my salary by dividing it immediately after receiving it through UnionBank .

Then I separate the money into different accounts:

- 50% goes to MariBank for savings and future goals.

- 35% goes to GoTyme Bank for family support and home renovation.

- 5% goes to Maya for emergencies.

- 10% goes to GCash for guilt-free spending.

The goal is not to copy someone else’s exact percentages. The goal is to give every part of your paycheck a purpose before it disappears into random spending.

Quick Navigation

- My monthly salary breakdown

- Why this budget works for my lifestyle

- A realistic salary budgeting example

- How I separate my money

- Budgeting mistakes I had to stop making

- Why I save 50% of my salary

- Why family gets 35%

- Why I still keep guilt-free spending

- Why I still keep an emergency fund

- Warning signs your budget is not sustainable

- How to create your own budget system

- What budgeting taught me

- Budgeting tools that helped me stay consistent

- References & financial resources

- Related tools

- Related guides

My Monthly Salary Breakdown

This is the exact paycheck budgeting system I personally follow every month.

I divide my salary immediately instead of waiting until the end of the month to see what is left.

Example of how I personally divide my salary each month between savings, family support, emergency money, and guilt-free spending.

| Category | Percentage | Purpose |

|---|---|---|

| Savings & Future Goals | 50% | Long-term goals and financial stability |

| Family & Home Renovation | 35% | Helping family and improving our home |

| Emergency Fund | 5% | Unexpected expenses and emergencies |

| Guilt-Free Spending | 10% | Personal enjoyment without guilt |

If you want to create your own system, you can use a monthly budget calculator or a 50/30/20 budget calculator as a starting point.

Why This Budget Works for My Lifestyle

One thing I realized very quickly is that budgeting advice online often assumes everybody has the same responsibilities, income level, and living situation.

But budgeting while living with parents looks very different from budgeting alone, supporting children, paying rent in a major city, or handling debt payments every month.

That is why I stopped trying to copy “perfect” budgeting percentages from the internet and started building a system around my actual life instead.

What made the biggest difference for me: I stopped asking “What is the best budget?” and started asking “What budget can I realistically maintain every month without burning out?”

Because my living expenses are currently lower, I decided this season of life was the best opportunity to focus heavily on saving money and helping my family while I still could.

I also noticed that budgeting became much easier once I accepted that some categories matter more to me than others.

For example, I honestly care more about:

- building long-term financial stability,

- supporting my family,

- reducing money anxiety,

- and avoiding unnecessary lifestyle inflation.

Once my spending started reflecting those priorities, budgeting stopped feeling restrictive and started feeling intentional.

A Realistic Salary Budgeting Example

A lot of budgeting advice sounds good in theory until you actually try to apply it to a real paycheck.

So here is what my percentage system could look like with a realistic monthly salary example.

| Budget Category | Percentage | Example Amount (₱35,000 Salary) |

|---|---|---|

| Savings & Future Goals | 50% | ₱17,500 |

| Family & Home Renovation | 35% | ₱12,250 |

| Emergency Fund | 5% | ₱1,750 |

| Guilt-Free Spending | 10% | ₱3,500 |

Seeing the actual numbers helped me understand whether my budget was realistic or not.

Sometimes percentages sound small until you calculate the real peso amount every month.

One mistake I used to make was creating a budget that looked good on paper but was impossible to maintain emotionally in real life.

That is why I think monthly budget planning should always consider both numbers and behavior.

How I Separate My Money

One of the biggest things that helped me stay consistent with budgeting was separating my money into different apps and accounts.

Before doing this, all my money stayed in one account and it became way too easy to overspend.

Now every part of my salary already has a job.

| Bank / App | Purpose | Referral / Code |

|---|---|---|

| UnionBank | Salary Account | Code: UBNOW-CCKWABER |

| MariBank | Savings & Future Goals | Get ₱150 with Code CP661878 |

| GoTyme Bank | Family & Home Renovation | Code: GOTYPH2XXX |

| Maya | Emergency Fund | Get ₱50 with Code @clarissa0225 |

| GCash | Guilt-Free Spending | Personal spending wallet |

Keeping my savings in MariBank helps me avoid touching the money impulsively.

My family and home renovation budget stays inside GoTyme Bank so I can clearly separate it from my personal money.

My emergency money stays in Maya because I do not want to accidentally spend it.

And my guilt-free spending stays inside GCash so I can enjoy it without feeling guilty afterward.

Budgeting Mistakes I Had to Stop Making

One reason many people struggle with personal finance is not because they are lazy or irresponsible.

Sometimes the real problem is that their budgeting system was never realistic to begin with.

Keeping everything in one account

This made it too easy for me to accidentally spend money meant for savings or emergencies.

Trying to budget perfectly

I used to feel guilty every time my spending was not “perfect,” which made budgeting emotionally exhausting.

Ignoring small spending

Coffee, delivery fees, subscriptions, and random convenience spending added up faster than I expected.

Saving whatever was left

This rarely worked because there usually was not much left at the end of the month.

The biggest improvement happened when I started treating saving money like a required expense instead of an optional leftover category.

Why I Save 50% of My Salary

Some people might think saving 50% is extreme, but I see it as taking advantage of an opportunity while I still can.

Living with my parents gives me the ability to save more aggressively than many people my age who already handle rent and full household expenses independently.

I did not want to waste that opportunity through lifestyle inflation and unnecessary spending.

- Saving gives me peace of mind.

- Saving gives me future flexibility.

- Saving helps me prepare for long-term goals.

- Saving reduces financial anxiety.

If you are trying to decide how much to save from your paycheck, this guide on how much you should save each month can also help.

Why Family Gets 35%

This is the most personal part of my budget.

Since I still live with my parents, I wanted to contribute financially in a meaningful way instead of simply keeping all my income for myself.

Part of my salary goes toward our home renovation and other family-related needs.

Helping improve our home feels more meaningful to me than buying random things I probably will not even care about months later.

My parents gave me stability, support, and a place to live. Contributing back feels important to me.

Why I Still Keep Guilt-Free Spending

One thing I learned about budgeting is that being too strict usually backfires.

That is why I intentionally keep 10% for guilt-free spending.

This is the money I can use for:

- coffee,

- eating out,

- small shopping purchases,

- hobbies,

- or spontaneous plans.

A sustainable budget should still allow you to enjoy your life.

This is also one reason many budgets fail. If a budget feels too restrictive, people often abandon it completely. That is why I liked this guide on why most budgets fail and how to fix yours .

Why I Still Keep an Emergency Fund

Even though I already save aggressively, I still separate money specifically for emergencies.

Unexpected expenses happen to everyone:

- medical expenses,

- urgent repairs,

- family emergencies,

- or unstable income periods.

Even a small emergency fund creates a financial buffer between stress and panic.

If you are still building your emergency savings, you can estimate a target using the emergency fund calculator .

Warning Signs Your Budget Is Not Sustainable

I think one of the most overlooked parts of budgeting is emotional sustainability.

A budget can technically “work” mathematically while still failing in real life because it feels impossible to maintain.

You constantly feel deprived

If your budget removes every enjoyable purchase, burnout usually happens eventually.

You keep restarting your budget

Constantly abandoning your system usually means something about it is unrealistic.

You avoid checking your finances

Avoidance often signals stress, guilt, or lack of clarity around spending.

Budgeting should reduce financial stress over time, not create constant anxiety every single month.

How to Create Your Own Budget System

If you are trying to create a budget for the first time, I honestly think simplicity works better than overly complicated spreadsheets.

The goal is not to build the most advanced budget system possible.

The goal is to create something you can realistically follow every month.

Calculate your real monthly income

Use your average income if your salary changes monthly instead of relying only on your highest earning months.

List your non-negotiable expenses

Include transportation, bills, debt, groceries, family support, and recurring payments.

Create savings categories first

I personally think saving becomes easier when it happens automatically before spending.

Leave room for real life

A sustainable budget should still include room for enjoyment, hobbies, social activities, or occasional spontaneous spending.

If you need help estimating your monthly expenses or savings goals, you can also use the monthly budget calculator and savings goal calculator .

What Budgeting Taught Me

Budgeting taught me that money management is less about restriction and more about clarity.

Before budgeting, money disappeared too easily because I never gave it a purpose.

Now every percentage already has a role before I even start spending.

This system helped me:

- become more intentional,

- reduce impulse spending,

- feel less anxious about money,

- and focus more on long-term goals.

Budgeting Tools That Helped Me Stay Consistent

One thing that helped me take budgeting more seriously was making the process easier and more visible.

I noticed that the harder a budgeting system feels to maintain, the easier it becomes to ignore.

Monthly Budget Calculator

Helpful for estimating monthly spending categories and creating a realistic monthly budget.

Emergency Fund Calculator

Useful for setting savings targets instead of guessing how much emergency money you need.

Expense Tracking

Tracking spending helped me notice small habits that quietly drained money every month.

Separate Bank Accounts

Separating money reduced impulse spending because each category already had a specific purpose.

Frequently Asked Questions

How should I budget my salary while living with parents?

A good salary budget while living with parents should reflect your real responsibilities, savings goals, family contribution, emergency fund, and personal spending.

Since housing costs may be lower, some people choose to save more aggressively, help support family expenses, or prepare financially for future goals.

How do I budget my paycheck?

You can budget your paycheck by dividing it immediately after receiving it and assigning money to savings, family support, emergency money, bills, debt, and personal spending before spending casually.

Is saving 50% of your salary realistic?

Saving 50% of your salary can be realistic if your expenses are low and you are not responsible for large monthly bills like rent or debt payments.

However, the ideal savings percentage depends on your income, location, lifestyle, and financial responsibilities.

Why separate salary into different bank accounts?

Separating money into different accounts helps make budgeting easier because each account already has a clear purpose.

It can also reduce impulse spending because savings, emergency money, family support, and personal spending are not mixed together.

Should I keep guilt-free spending in my budget?

Yes. Keeping a guilt-free spending category can make budgeting more sustainable because it allows you to enjoy part of your income without feeling restricted all the time.

What is the best budgeting method for beginners?

The best budgeting method is the one you can consistently follow.

Many beginners start with percentage-based budgeting systems like 50/30/20 or paycheck budgeting because they are simple and easy to maintain.

Should you save aggressively while living with parents?

Many people choose to save more aggressively while living with parents because housing and utility costs may be lower during that stage of life.

For some people, it becomes an opportunity to build an emergency fund, prepare for moving out, reduce debt, or improve long-term financial stability earlier.

Why does budgeting feel emotionally difficult sometimes?

Budgeting can feel emotionally difficult because spending habits are often connected to stress, comfort, social pressure, convenience, or lifestyle expectations.

That is why sustainable budgeting usually works better than overly restrictive budgeting.

References & Financial Resources

This guide is based primarily on personal budgeting experience and practical money management habits.

Additional budgeting concepts referenced throughout this article are commonly discussed in:

- Consumer budgeting frameworks

- Emergency fund planning principles

- Zero-based and percentage budgeting systems

- Behavioral finance and spending psychology

- Personal savings strategies

Financial situations vary significantly depending on income, location, debt, family responsibilities, and cost of living. Readers should adjust any budgeting percentages based on their own circumstances.

Important Note

This article is based on personal experience and is for educational purposes only.

Some links to banks, wallets, or financial apps may be referral or affiliate links. LifeToolSuit may earn a small reward if you sign up through those links at no extra cost to you.